.jpg&w=1920&q=75)

President Donald Trump confessed during the G7 summit in France that continuing the Iran war would have created an "economic catastrophe." Resolving the conflict was imperative to limit the risk of a recession, depression, or anything in between, fueled by soaring global energy prices. And there lies the rub: Was the memorandum of understanding a defeat for the Tehran regime, or a measure to reduce risk? The data presents critical findings.

Oil Fallout in the Iran War

Who knows what is happening between the United States and Iran? Vice President JD Vance assured everyone during a Swiss news conference that the situation was proceeding as expected. President Donald Trump stated Washington could restart the bombing if an agreement is not finalized. Tehran keeps sending mixed messages: The Strait of Hormuz is closed one day and open the next.

The longer the war drags on, the worse it will be for the global economy. “We run out of reserves at about four weeks. You know, there are reserves all over the world, and we would really run out, and there’ll be a time when you wouldn’t be able to get it. It would be bedlam,” Trump said overseas.

Various banks and oil companies ostensibly agree, presenting various price forecasts. JPMorgan Chase said Brent, the global benchmark for oil prices, could hit $130 if disruptions persist. Goldman Sachs estimated Brent reaching triple digits for months. Exxon, pointing to historically low global inventories, said the secondary effects could push a barrel of crude to around $130.

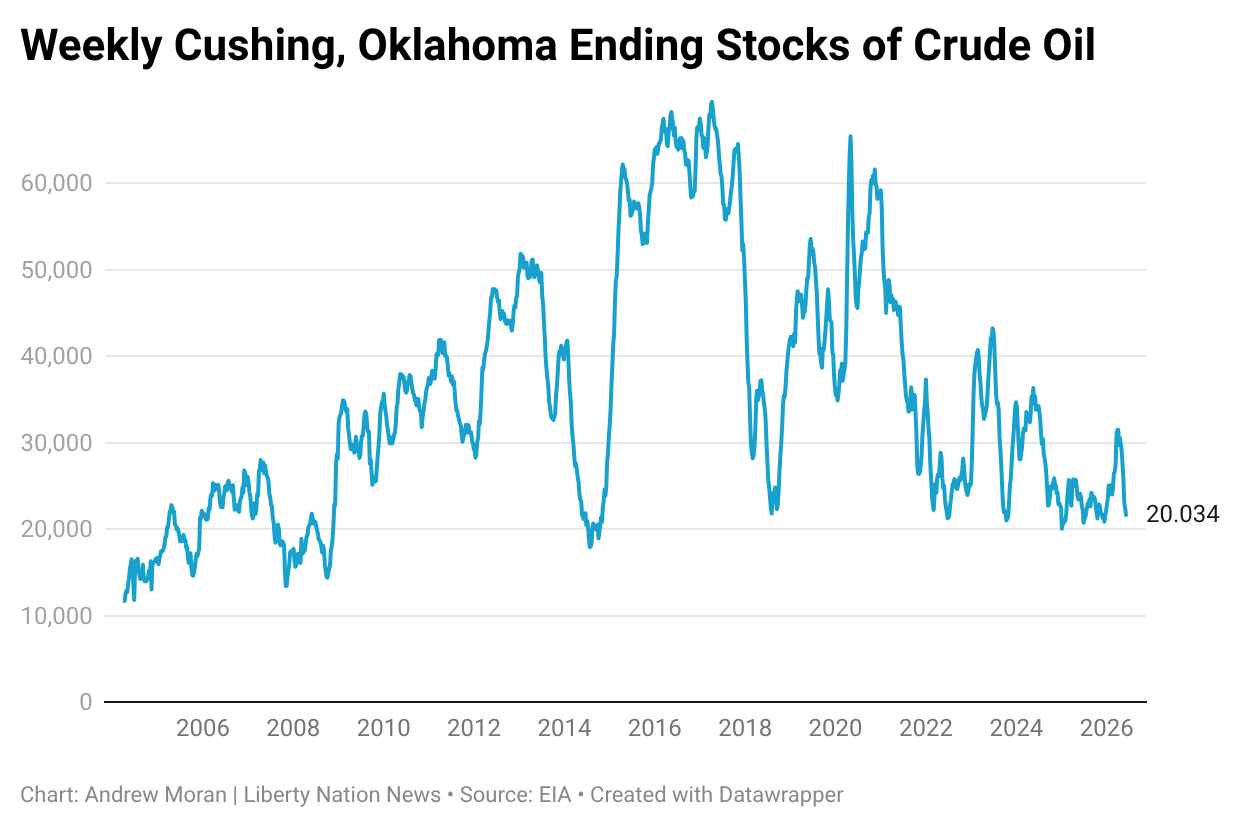

Oil stockpiles have been diminishing at home and abroad.

Cushing, Oklahoma storage (excluding Strategic Petroleum Reserves) sits at around 20 million barrels, the lowest since 2014, according to the US Energy Information Administration. The International Energy Agency noted in its latest report that global observed inventories declined by 143 million barrels in May, equivalent to more than 4 million barrels per day.

"OECD government inventories fell by 163 mb (-1.8 mb/d) over the same period to their lowest level since December 1990 as the pace of emergency stock releases accelerated," the organization stated.

Chevron CEO Mike Wirth told Bloomberg Television last week that the adverse effects from prolonged disruptions in the Middle East could be realized in July or August. "That’s the real question is: 'How much longer can these measures kind of ameliorate the risk?'" Wirth said. "At some point, they may not be able to."

Suffice it to say, the current administration likely saw the writing on the wall and attempted to put together a deal. Whether it will be good or bad will be left up to the political pundits.

Not All Bad News

The Iran war could be a black eye on President Trump's legacy. At the same time, the conflict has led to records and opportunities for America's energy industry.

First, the United States is producing crude oil more than ever before, inching closer to 14 million barrels per day, up from 13.431 million barrels per day the previous year. Additionally, energy firms could be bracing for higher-for-longer oil prices as the Baker Hughes rig count is at a one-year high of 433, signaling more production ahead.

Second, US petroleum exports are surging as the world wants what America has. Shipments are at an all-time high, which is positive for growth prospects, as exports contribute to gross domestic product (GDP) calculations.

Finally, the Treasury Department authorized the sale of dollar-denominated Iranian oil and fuel under a 60-day license, opening the door for America to purchase Tehran's Texas Tea and other petroleum and petrochemical products. US refineries, which are at maximum capacity, could also be busy refining the light, sweet crude from the Middle East.

Worried

So far, the global economy does not appear to be on the brink of catastrophe. Indeed, central banks are losing sleep over an inflation revival, with institutions raising interest rates or keeping them higher for longer. But the consensus, at least on the other side of a potential memorandum of understanding, is that oil prices will plummet due to a flood of supply traversing global markets, slowing demand, and larger output.

.jpg&w=1920&q=75)

.jpg%20Food%20Inflation&w=1920&q=75)